Section 2 of 7

Export Documentation: Getting the Paperwork Right

Why documentation matters more than most exporters realise

Most exporters understand that documentation matters. What is less well understood is the scale of what can go wrong when it falls short — and how far the consequences can reach.

Your paperwork is not a formality that follows the commercial deal. It is what customs authorities use to assess and clear your goods. It is what your buyer needs to get their shipment through their own border. It is what HMRC will ask to see if they audit you. And it is what insurers will examine if a claim is made.

Getting documentation wrong can result in goods being held at a port, duty being assessed incorrectly, or preference being denied at the buyer’s end. Poor documentation habits also create a specific VAT risk: exports are zero-rated for UK VAT purposes, but that zero-rating has to be substantiated. If HMRC audits you and you cannot produce adequate proof that the goods left the UK, you may be required to account for VAT on those sales retrospectively.

The good news is that the same core set of documents underpins almost every export. Understanding what each one is, what it needs to contain, and why — gives you the foundation to get it right every time.

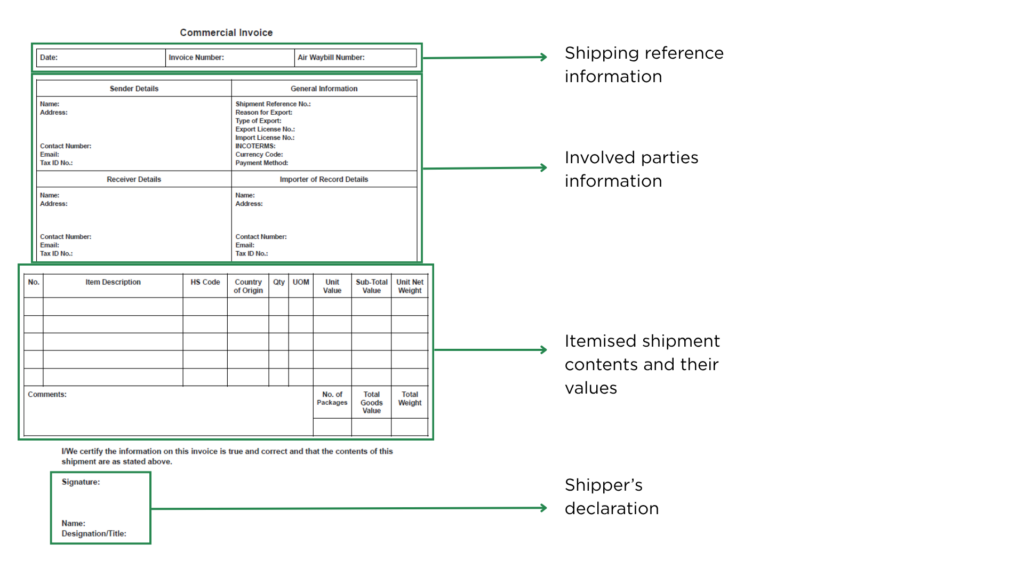

The commercial invoice — your most important document

The commercial invoice is the central document in any export. Every other document either references it or is built on the information it contains. It is used by customs authorities to assess the goods and calculate duty, by freight forwarders to complete the export declaration, and by your buyer to clear the goods at their end.

A commercial invoice is not the same as a domestic invoice. It needs to contain significantly more information — and that information needs to be accurate.

At minimum, a compliant export commercial invoice will include the seller and buyer details, a specific description of the goods, the commodity code, country of origin, accurate value and currency, weights and dimensions, the agreed Incoterm, payment terms, and any required declarations such as a preference statement.

The goods description needs to be specific enough for a customs officer unfamiliar with your product to understand what it is. What that means in practice varies enormously by product, and getting it wrong — even with good intentions — can cause a shipment to be held or a declaration to be queried.

The value has more ways to go wrong than most exporters realise: rounded figures, transfer prices that don’t reflect true transaction value, freight and insurance costs that should or shouldn’t be included depending on the Incoterm agreed, and the particular challenge of free-of-charge shipments — samples, warranty replacements, repairs — where the invoice still needs to show a realistic customs value even though no sale has taken place.

The Incoterm is not just a label to add at the bottom of the document. The Incoterm agreed between you and your buyer determines what other information the invoice needs to contain — and some of those requirements are ones that catch experienced exporters out, not just those doing it for the first time.

The packing list — the commercial invoice’s best friend

While the commercial invoice tells customs what the goods are worth and who is buying and selling them, the packing list tells everyone involved what is physically in the shipment, where it is, and how it is packed. This matters at customs, where officers may need to inspect specific items. It matters to your buyer, who needs to locate and check what they have received. And it matters in the event of damage or loss, where an accurate packing list can be the difference between a successful insurance claim and a disputed one.

A good packing list should be clear, specific, and tied back to the commercial invoice. It should include:

- The origin and destination of the goods

- The commercial invoice number for cross-reference

- The total number of packages in the shipment

- Details for each individual package: its contents, weight, and dimensions

- The total gross and net weight for the shipment

- Exporter and consignee contact details

- The shipping mark — the reference visible on the outside of the packaging that ties the physical item to the paperwork

Packing lists should be sent to your buyer before the goods are shipped, so they can check the contents and raise any discrepancies before the goods are in transit. This sounds obvious, but it is frequently skipped — and the consequences are avoidable.

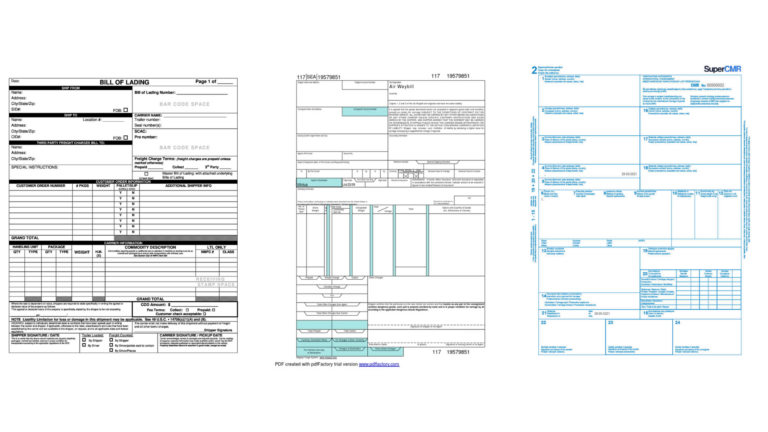

Transport documents — proof that the goods moved

Transport documents serve a dual purpose. They are the contract of carriage between you and the carrier, confirming that the goods have been handed over for transport. But when correctly authenticated, they also serve as commercial proof of export — one of the two main forms of evidence HMRC will accept to confirm that goods left the UK.

The type of document depends on how the goods are moving. Sea freight uses a Bill of Lading, issued by the shipping line. Air freight uses an Airway Bill, issued by the airline or, where a freight forwarder is consolidating shipments, by the forwarder itself. Road freight uses a CMR — a consignment note governed by an international convention incorporated into UK law. Each works differently, carries different legal weight, and has different requirements for it to be considered authenticated.

One document that is frequently misunderstood is the courier waybill. It is a contract of carriage, but it is not a transport document in the legal sense and cannot on its own serve as proof of export. When goods move via courier, proof of export comes from the Proof of Delivery — the delivery signature, timestamp, and location available through the courier’s tracking system. This needs to be downloaded and saved at the time of delivery. Many couriers remove or archive this data within a few months, long before the six-year retention period HMRC requires.

Proof of export — what HMRC actually needs

The concept of proof of export matters because exports are outside the scope of UK VAT. To treat a sale as zero-rated, HMRC requires evidence that the goods genuinely left the UK within 90 days of the time of supply. Without that evidence, you may be required to account for VAT on the sale retrospectively — together with financial penalties.

HMRC accepts two categories of export evidence.

Official evidence is the Full Entry Printout from the Customs Declaration Service (CDS) — the electronic record generated when the export declaration is submitted and cleared. This is issued against your EORI number and is the clearest form of proof. The challenge is obtaining it: freight forwarders are under no legal obligation to provide it automatically, and some are slow or reluctant to do so. You should request it in writing for every shipment as a matter of routine.

Commercial evidence includes authenticated transport documents — the Bills of Lading, Airway Bills, and signed CMRs described above. These hold equal weight to the CDS printout, provided they are supported by supplementary evidence.

Supplementary evidence is the paper trail that ties the transaction together: the purchase order, the commercial invoice, the packing list, evidence of payment, and any correspondence relating to the shipment. HMRC wants to be able to see, in the event of an audit, that the goods you invoiced are the goods that were declared, are the goods that were shipped, and are the goods that arrived at the destination.

The 90-day rule catches more exporters out than almost anything else in this area. HMRC requires that goods physically leave the UK within 90 days of the time of supply in order for the export to be treated as zero-rated. The time of supply — known as the tax point — is whichever comes first: the date the goods are sent or collected, or the date the buyer pays in full. If payment arrives well ahead of shipment, the 90-day window may already be running before the goods have left the building. Records must be retained for six years plus the current tax year.

Certificates of origin — proving where your goods come from

A certificate of origin is a document that formally declares the country in which goods were produced, manufactured, or substantially processed. There are two distinct types, and they serve different purposes.

Non-preferential certificates of origin are typically requested by the buyer or required by the destination country for customs, regulatory, or commercial reasons. They are commonly requested by buyers in countries including China, India, Pakistan, and across the Middle East — and for Middle Eastern markets in particular, there are specific certificate types and additional steps, including in some cases legalisation by the relevant embassy. In the UK, these certificates are issued by Chambers of Commerce.

Preferential certificates of origin are used where the UK has a trade agreement with the destination country and the goods meet the rules of origin set out in that agreement. Getting this right allows the buyer to claim reduced or zero import duty — which can make a real commercial difference to the cost of doing business with you. Whether your goods qualify, which document applies, and what you need to do to evidence it correctly is where the detail and the risk sits.

Additional documentation — when the standard set is not enough

For most standard commercial shipments, the commercial invoice, packing list, and transport document cover the basics. But depending on your goods, your buyer’s requirements, and the destination country, additional documentation may be needed — and the consequences of not having it in place before the goods move range from delays at the border to shipments being refused entry entirely.

Pre-shipment inspections are required by some countries or buyers as a condition of entry or payment. They need to be arranged well in advance — waiting until the goods are ready to ship is too late.

Certificates of conformity are required by countries with national conformity assessment programmes, where imported goods must meet specific technical or safety standards. Requirements vary significantly by country and by product category.

Export health certificates are official UK government documents required for exports of animals, animal products, and many food and drink categories. These are not buyer-driven — they are a legal requirement in many markets, and goods without them will not clear the border.

The starting point for checking what your specific goods and destination require is the government’s Check Duties and Customs Procedures tool — a genuinely useful resource that most exporters have never heard of.

Common documentation mistakes — and what they actually cost

Vague goods descriptions. Customs authorities need to be able to identify goods from the invoice alone. “Parts,” “components,” or “goods as per order” are not acceptable descriptions. The description must be specific enough to allow classification.

Wrong or missing commodity codes. The commodity code on the export declaration determines whether an export licence is required, whether the goods attract any restrictions, and how the rules of origin are applied. If the code on the invoice and the declaration do not match, everything downstream may also be wrong.

Incorrect values. Whether the error is a rounded figure, a value in the wrong currency, or a transfer price rather than a true market value, an inaccurate value on the commercial invoice creates customs compliance risk at both ends of the shipment.

Incoterm not stated, or the wrong Incoterm stated. The Incoterm affects who holds responsibility for the goods at each stage of transit, who arranges and pays for freight and insurance, and when the time of supply begins. A missing or incorrect Incoterm is not just a documentation gap — it is a contractual and compliance issue.

No proof of export retained. Businesses export, dispatch the goods, and file the invoice — but never obtain, store, or organise the evidence that the goods left the UK. This is perhaps the most common serious error in UK export compliance.

Relying on the courier to hold your records. Courier tracking data disappears. PODs are archived. If you do not download and save proof of delivery at the time it is available, it may be gone before you need it.

Want to build your confidence with documentation?

Our Getting Commercial Invoices and Packing Lists Right course gives you the hands-on knowledge to produce accurate, compliant documentation with confidence. Our Guide to Exporting and Export Documents course covers the full document set in a one-day session.

View All CoursesWant someone to check — or handle — your documentation?

Our Compliance Healthcheck reviews your existing paperwork and process against HMRC requirements. Our Outsourced Shipping Department and Customs Declarations services take that responsibility off your hands entirely.

Find Out About Our Export ServicesThe Complete Guide to Exporting from the UK

- 01 — Understanding the Export Process

- 02 — Export Documentation You are here

- 03 — Customs, Declarations & Commodity Codes

- 04 — Incoterms® 2020 & Contracts

- 05 — Trade Agreements, Rules of Origin & Reducing Duties

- 06 — Getting Paid & Managing Financial Risk

- 07 — Export Controls & Licensing