Section 1 of 7

Understanding the Export Process

What does exporting actually mean?

At its most straightforward, an export is the movement of goods outside of the UK. But that simple definition carries a significant amount of legal and practical weight — more than most businesses anticipate before they begin.

When goods leave the UK for an overseas buyer, a specific set of obligations comes into play regardless of what you’re shipping, where it’s going, or how experienced you are:

- A customs declaration must be submitted into HMRC’s Customs Declaration Service (CDS) — this is a legal requirement, not optional

- The sale falls outside the scope of UK VAT — which is advantageous, but requires you to handle it correctly

- You must be able to prove the export took place, in the event of an HMRC audit

These obligations apply whether you’re shipping a single pallet to a customer in France or a full container to a distributor in Singapore. The scale changes. The requirements don’t.

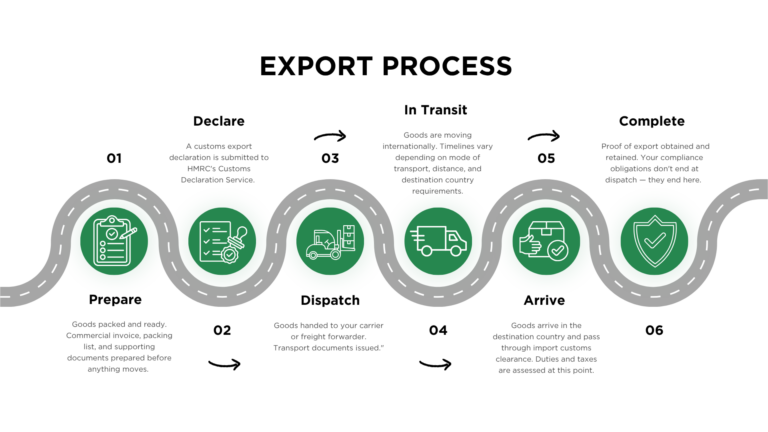

The export journey end to end

Understanding the shape of the export process — before getting into the detail of any individual step — is the single most useful thing you can do when you’re starting out, or when you want to identify where your current process might have gaps.

A few things worth understanding about this process before we get into each stage:

Documentation comes before the goods move. Your paperwork — the commercial invoice, packing list, and customs declaration — isn’t something you sort out once the goods are on the truck. It’s what authorises the movement in the first place. Getting the sequence right matters.

Someone has to make the customs declaration — and the responsibility for its accuracy is real. Whether that’s you, a freight forwarder, or a customs broker acting on your behalf, a declaration must be submitted. Whoever is named as the exporter of record carries legal liability for what’s in it. Understanding what that means for your business — especially if you’re currently relying on a third party without fully understanding what they’re submitting — is more important than many exporters realise.

The process doesn’t end when the goods leave your warehouse. Your buyer will need to clear the goods through customs in their own country, pay applicable duties and taxes, and take legal title at a specific point in the journey. Where that point is — and who’s responsible for what up to that moment — depends on the Incoterm you’ve agreed with your buyer. This is where a surprising number of costly misunderstandings originate.

Proof of export is your protection, and it has to be collected proactively. If HMRC audit your VAT records, you’ll need to demonstrate that goods physically left the UK. What constitutes valid proof, and how to make sure you’re collecting it consistently, is something every exporting business needs to have nailed down before shipments move — not after.

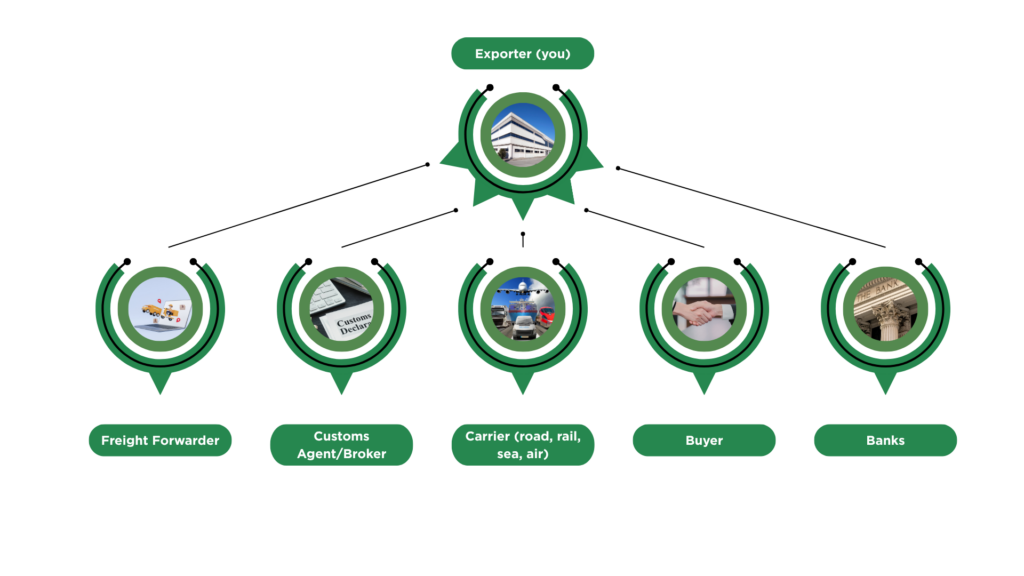

The key parties in an export

Depending on how you’re set up, what you’re shipping, and where it’s going, several different parties will be involved in getting your goods from your premises to your overseas customer. Knowing who does what — and where your responsibilities end and theirs begin — is essential.

The five most common — and costly — export mistakes

Misclassifying goods. Every product exported from the UK must be assigned a commodity code — an internationally standardised classification number that tells customs what the goods are. The code determines the duty rate your buyer pays, the documentation that’s required, and in some cases whether an export licence is needed. Getting it wrong has consequences on all three fronts, for both you and your buyer. We cover commodity codes in detail in Section 3.

Errors on the commercial invoice. The commercial invoice is the single most important document in an export shipment. It’s the basis for the customs declaration, the proof of the transaction’s value, and often the document against which payment is made or verified. Errors — in the goods description, declared value, country of origin, or the specific information required by the destination country — can stop a shipment at the border, trigger delays, and in some cases result in the goods being held or returned. What a compliant commercial invoice must contain is covered in Section 2.

Choosing the wrong Incoterm. The Incoterm you agree with your buyer defines who is responsible for transport, insurance, customs clearance, and risk at every stage of the journey. It also has direct implications for your proof of export, your VAT position, and your practical ability to manage the shipment. Many UK exporters default to terms that appear to simplify their obligations — without fully understanding the problems that choice can create downstream. The 11 Incoterms 2020 rules are covered in Section 4.

Failing to collect proof of export. If you’ve treated an export sale as outside the scope of UK VAT — which is correct — you need to be able to prove to HMRC that the goods actually left the UK. Valid proof of export comes from specific documents, and it needs to be collected at the time of shipment. Many exporters don’t fully understand what constitutes valid proof, or they assume that because a freight forwarder is involved, it’s being handled. That assumption isn’t always safe.

Overlooking export controls. Certain goods — including some technologies, software, chemicals, and goods with potential dual-use or military applications — require a licence before they can be exported. This applies regardless of their intended end use, and regardless of whether the exporter was aware of the requirement. Exporting controlled goods without the appropriate licence isn’t a paperwork oversight — it’s a criminal offence. Export controls are covered in Section 7.

Why this matters before the detail

This section has deliberately stayed at the level of the whole picture. Before working through the specifics of documentation, commodity codes, Incoterms, and payment — you need to understand the journey those details sit within, and why each piece exists.

Exporters who handle this well tend not to be the ones who know the most rules. They’re the ones who understand the process end to end, know where their responsibilities lie, and have built the right knowledge and support around the areas where the stakes are highest.

The sections that follow go into the depth you’ll need on each part of that journey. And if, as you read, you’re finding that some of these areas are less well understood in your business than they should be — that’s a very normal position to be in, and exactly what our training is designed to address.

Want to learn this in practice?

Our Guide to Exporting and Export Documents course covers the full export process in a structured session — real examples, practical exercises, and space to ask questions specific to your business. Available as a scheduled public course or as private in-house training.

View Course DatesWant us to handle this for you?

Our Outsourced Shipping Department service manages the export process on your behalf — declarations, documentation, and day-to-day compliance — so your team can focus on the business.

Find Out MoreThe Complete Guide to Exporting from the UK

- 01 — Understanding the Export Process You are here

- 02 — Export Documentation

- 03 — Customs, Declarations & Commodity Codes

- 04 — Incoterms® 2020 & Contracts

- 05 — Trade Agreements, Rules of Origin & Reducing Duties

- 06 — Getting Paid & Managing Financial Risk

- 07 — Export Controls & Licensing